Gamma distribution

The gamma distribution is a flexible continuous distribution that generalizes the exponential. While the exponential models the waiting time until the first event, the gamma models the waiting time until the \(k\)-th event in a Poisson process.

Definition

A random variable \(X\) follows a gamma distribution with shape parameter \(k > 0\) and rate parameter \(\lambda > 0\), written \(X \sim \text{Gamma}(k, \lambda)\), if its PDF is:

\[f(x) = \frac{\lambda^k x^{k-1} e^{-\lambda x}}{\Gamma(k)}, \quad x > 0\]

where \(\Gamma(k) = \int_0^\infty t^{k-1} e^{-t}\, dt\) is the gamma function. For positive integers, \(\Gamma(k) = (k-1)!\). For example, \(\Gamma(3) = 2! = 2\) and \(\Gamma(5) = 4! = 24\).

An equivalent parametrization uses the scale parameter \(\theta = 1/\lambda\):

\[f(x) = \frac{x^{k-1} e^{-x/\theta}}{\Gamma(k)\, \theta^k}, \quad x > 0\]

⚠️ Parametrization: rate vs scale - check your software

The gamma distribution is parametrized in two common ways:

- Rate (\(\lambda\)): R uses

dgamma(x, shape = k, rate = lambda). Mean \(= k/\lambda\). - Scale (\(\theta = 1/\lambda\)): R also accepts

dgamma(x, shape = k, scale = theta). Mean \(= k\theta\).

Python’s scipy.stats.gamma uses shape \(k\) and scale \(\theta\). Always verify which convention your source uses before computing probabilities.

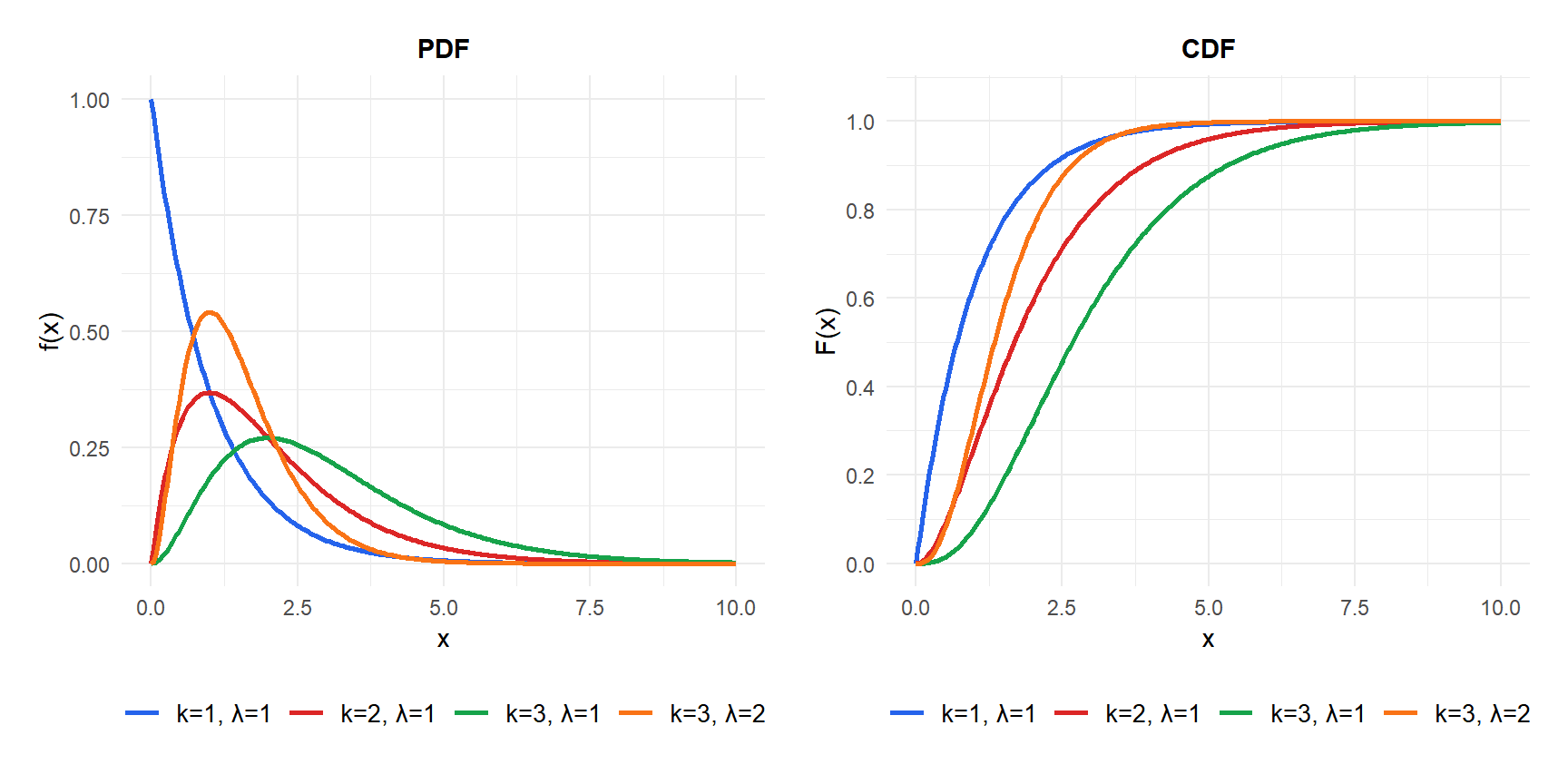

Probability Density Function and CDF

The CDF is expressed via the lower incomplete gamma function:

\[F(x) = \frac{\gamma(k,\, \lambda x)}{\Gamma(k)}\]

where \(\gamma(k, u) = \int_0^u t^{k-1} e^{-t}\, dt\). There is no closed form for general \(k\); probabilities are computed numerically.

Properties

For \(X \sim \text{Gamma}(k, \lambda)\):

- Expected Value (Mean)

\[E(X) = \frac{k}{\lambda}\]

- Variance

\[\text{Var}(X) = \frac{k}{\lambda^2}\]

- Skewness

\[\text{Skewness} = \frac{2}{\sqrt{k}}\]

The distribution is right-skewed for small \(k\) and becomes increasingly symmetric as \(k\) grows. For large \(k\), the gamma approaches a normal distribution.

- Kurtosis

\[g_2 = \frac{6}{k}\]

- Mode

\[\text{Mode} = \frac{k-1}{\lambda} \quad \text{for } k \geq 1\]

For \(k < 1\), the distribution is monotonically decreasing and the mode is 0.

- Quantile Function

No closed form; computed numerically.

Special cases

The gamma distribution unifies several important distributions:

- Exponential: \(\text{Gamma}(1, \lambda) = \text{Exp}(\lambda)\). The waiting time until the first event.

- Erlang: \(\text{Gamma}(k, \lambda)\) with \(k\) a positive integer. The waiting time until the \(k\)-th event in a Poisson process with rate \(\lambda\).

- Chi-squared: \(\text{Gamma}(\nu/2,\, 1/2) = \chi^2(\nu)\). Fundamental in hypothesis testing and confidence intervals.

If \(X_1, X_2, \ldots, X_k\) are independent \(\text{Exp}(\lambda)\) random variables, their sum:

\[S = X_1 + X_2 + \cdots + X_k \sim \text{Gamma}(k, \lambda)\]

This is the most intuitive interpretation: if each event takes an exponential waiting time, the total time until \(k\) events have occurred follows a gamma distribution.

Step-by-step example

A technical support team resolves tickets one by one. Each ticket takes an exponentially distributed time with mean 4 hours (\(\lambda = 1/4\)). What is the distribution of the total time to resolve 3 tickets?

\(X \sim \text{Gamma}(3,\, 1/4)\) (or equivalently, \(\text{Gamma}(k=3, \theta=4)\)).

Expected total time:

\[E(X) = \frac{3}{1/4} = 12 \text{ hours}\]

Variance and standard deviation:

\[\text{Var}(X) = \frac{3}{(1/4)^2} = 48 \text{ hours}^2, \qquad \text{SD}(X) = \sqrt{48} \approx 6.93 \text{ hours}\]

Probability of resolving all 3 tickets within 10 hours:

\[F(10) = P(X \leq 10) \approx 0.456\]

Computed numerically: pgamma(10, shape = 3, rate = 1/4) in R.

Probability of taking more than 15 hours:

\[P(X > 15) = 1 - F(15) \approx 1 - 0.677 = 0.323\]

About 32% of three-ticket sessions will take more than 15 hours.

Monthly rainfall (in mm) in a region follows a \(\text{Gamma}(3, 0.1)\) distribution (mean \(= 30\) mm, SD \(\approx 17.3\) mm).

- Probability of less than 20 mm:

pgamma(20, shape = 3, rate = 0.1)\(\approx 0.323\). - Median rainfall:

qgamma(0.5, shape = 3, rate = 0.1)\(\approx 26.5\) mm.

The gamma is frequently used for rainfall because it is always positive, right-skewed, and flexible in shape.

💡 Relationship with other distributions

- Exponential: \(\text{Gamma}(1, \lambda)\).

- Chi-squared: \(\text{Gamma}(\nu/2, 1/2)\), the basis of many hypothesis tests.

- Normal approximation: for large \(k\), \(\text{Gamma}(k, \lambda) \approx N(k/\lambda,\, \sqrt{k}/\lambda)\).

- Beta: if \(X \sim \text{Gamma}(\alpha, 1)\) and \(Y \sim \text{Gamma}(\beta, 1)\) independently, then \(X/(X+Y) \sim \text{Beta}(\alpha, \beta)\).

- Inverse gamma: if \(X \sim \text{Gamma}(k, \lambda)\), then \(1/X\) follows an inverse gamma, used as a prior for variance in Bayesian statistics.